For much of the financial advice industry’s history, advisers and investment managers have struggled with organic growth – not just how to achieve it but also how to define it and measure it. In this article, we explore why organic growth should be a high priority for financial advice firms. We’ll cover the following key topics: How we measure and define organic growth; what good organic growth looks like; some common approaches to improving organic growth.

Organic growth is a new concept in wealth management

To understand many advisers’ complex history with organic growth, one would need to trace the history of the industry back to its roots.

Some 20 years ago, most advisers were tied sales agents for large life insurance groups. Their income came from commissions on sales of products invested in life insurance structures. Tracking inflows and outflows was not a meaningful exercise because, first, end clients were contracted with product providers and life insurers — not with advisers. And second, commission payments were linked to original product/contract value with inflows and outflows having no meaningful impact on an adviser’s take-home pay.

Then, in 2013, the Retail Distribution Review outlawed commission payments and forced life insurers to open their trading infrastructures to third-party products. In response, advisers shifted towards a direct assets under management (AUM)-based fee model with their end clients. This change tied their fate to the ebb and flow of AUM.

The struggle for organic growth has been an ongoing issue in the industry, exacerbated since last year due to uncertain macroeconomic conditions and additional administrative burdens arising from Consumer Duty. Before that, the principal preoccupation of many advice firms, especially the larger national ones (variously called ‘aggregators’ or ‘consolidators’), was roll-up consolidation. Growth through acquisitions was deemed easier to achieve than was organic growth, and many shareholders actively encouraged rapid scale-build over capability-build in anticipation of a quick exit.

In previous insights, shared in our wealth management series, change in economic situations have pushed the topic of organic growth much higher up on the C-suites’ agenda. Investors in financial advice businesses are already spoiled for choice, with more than 40 private equity-backed UK advice firms competing for their money and attention. Why should they back one over another? What steps can be taken?

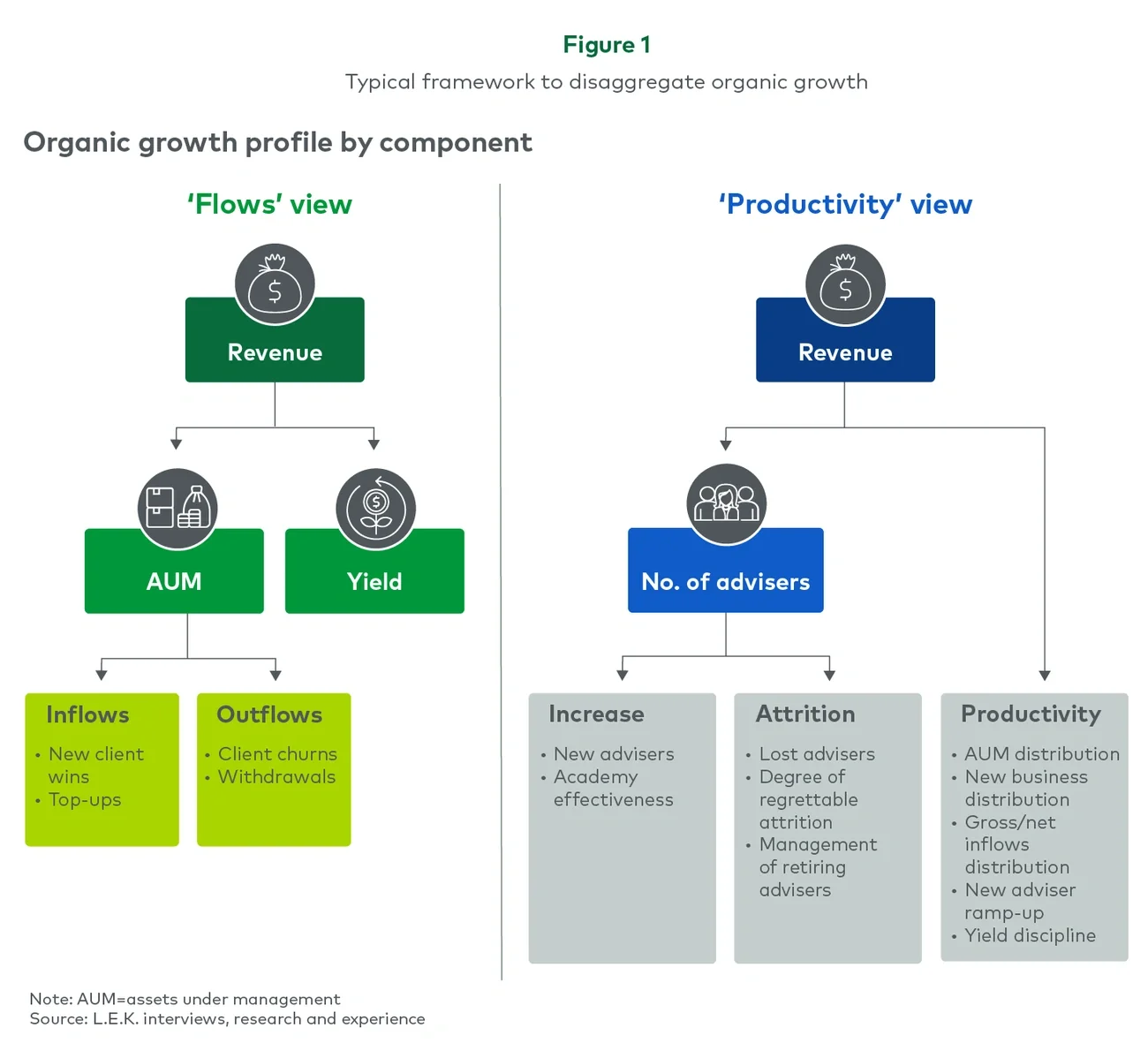

Step 1: Defining organic growth

What counts as organic growth — other than simply ‘not M&A’? At L.E.K. Consulting, we have a standard framework that helps our clients understand their organic growth profile (see Figure 1).